THE analysis in the last chapter of the sources of investment difficulties between capital-importing and capital-exporting countries ran in terms of a multiplicity of clearcut economic and cultural conflicts, any one of which might give rise, under the proper circumstances, to political friction. If the analysis of this present chapter is to be realistic it will have to be much less clear-cut, for only to a minor extent does investment friction between capital-exporting nations---which is to say, with slight inaccuracy, between great powers---arise directly out of investments or investment interests themselves. Rather, many complex factors of the sort commonly called political, historical, psychological, combine with other factors of the economic variety (among which investment interests may or may not play a rôle) to produce an opposition of interest or attitude between capital-exporting countries, and in this opposition of interest or attitude the private investments of citizens then become entangled.

Our job, therefore, is to analyze two sources of investment friction between capital-exporting countries: first, the creation of investment friction by the clash of immediate investment interests, including the immediate pressure of investors on the policies of capital-exporting states; second, the entanglement of investments in conflicts not immediately occasioned by them, but resulting from a complex in which investments may or may not be one among many contributing factors. The complex of factors which has most frequently brought private international investments into political friction we shall subsume under the term "expansionism."(2) It will therefore become imperative at some later stage in the analysis to examine the rôle of private investments in the origin of expansionism. This outlines the course of the present chapter.

There are two direct economic conflicts between rival lending groups which, like the conflicts examined in the last chapter, manifest themselves as domestic problems within the boundaries of national states and assume an international aspect when capital crosses frontiers. These are, first, the conflict of competing suppliers of capital for the most attractive investment opportunities, and, second, the conflict between joint creditors of the same debtor or debtor group as to precedence of claims, especially if the debtor's ability to repay in full becomes doubtful. A few years ago it could have been said that conflicts of this second sort seem never to have assumed any great importance in modern international politics, at least with respect to private investments, but one effect of the world depression has been to raise precisely such issues. It is the widespread resort to governmental control of foreign exchange, usually as a measure of monetary policy in the first instance, which has laid the basis for political supervision of outgoing private payments and thereby raised the question of discrimination in this regard. This has been noted in connection with the German private debts (Chapter 2). A long duration of depressed economic and financial conditions which make both domestic and foreign debt payments problematical, or continued developments in the direction of national control over economic life, would almost certainly have the effect of elevating this clash of interest between creditor groups into a first-rate problem of international politics.

The spotlight of attention in the past has rightly been concentrated, however, upon the international political effects of competition for investment opportunities. There is no doubt that the direct clash of economic interest between lending groups of different nationalities seeking to make placements abroad has been a factor in the origin of investment frictions between capital-exporting countries. But the reader should be warned against assuming that this direct clash of interest is in any sense a complete or adequate explanation of such investment frictions. In the first place, it fails to explain why the conflicts manifest themselves in the form of political friction between competing lenders of different national citizenship and not between competing lenders of the same national citizenship. A corrective to which those who discuss the "economic" causes of international friction can hardly resort too often is to remind themselves that the economic conflicts discovered in connection with these frictions often exist within single countries without giving rise to comparable results. In the present instance, competition for desirable investment opportunities in, let us say, the Far East, has existed between different British firms and different German firms in just as valid an economic sense as it has existed between British and German firms. An explanation of international investment friction must add non-economic elements to these purely economic conflicts of interest; it must give due weight to the psychology of nationalism and to the system of organization, or the lack of it, of relations between national political units.(3)

In the second place, the direct clash of interest between lending groups in search of investment opportunities is not a complete or adequate explanation of investment friction between capital-exporting countries because it fails to accord with the inductive evidence (developed in Chapter 13) that in cases of serious investment friction between great powers the private investments have characteristically been involved as tools of diplomacy, rather than as determiners of diplomacy. This inductive evidence does not prove that the economic conflict of interest between lenders, of which we have been speaking, has no causal connection with the investment frictions in question, but it does seem to establish rather definitely that the connection has not ordinarily been direct, proximate, immediate. The stream of causal influence which flows from lenders' conflicts of interest to international political friction over investment opportunities follows a devious channel, and is usually joined in its course by other streams of influence which modify or absorb it. Some of these other streams are: strategic considerations of national power in the broadest sense and of national defense in the narrower sense; economic beliefs and doctrines accepted by statesmen, whether sound or unsound; messianic visions in the cultural field, with accompanying drives to convert the heathen, spread civilization, or assume the white man's burden; competitive national efforts to find markets for industrial products; emotional drives for national prestige. All these factors and more may enter into international frictions between great capital-exporting powers; so that even when the friction centers about concessions, colonies, or other issues related to investment opportunities, the element of actual direct economic conflict may be very dilute.

All this may seem over-subtle and academic, but it makes a great practical difference for purposes of control whether one believes that the immediate impulse to dangerous frictions between capital-exporting powers comes from lending groups who find themselves in competition for desirable investment opportunities, or whether one believes that the immediate impulse is more likely to come from complexly motivated political ideas like the urge for national expansion, which ultimately may depend in part (but indirectly and only in part) upon investment interests, while immediately they use investments as a tool. The second view is much closer to the facts than the first, and conscious or unconscious acceptance of the first as a working hypothesis has made the suggestions of various reform groups much less useful than they might otherwise have been. The stakes which turn on the issue of international peace or war are so tremendous, and the margin by which it may be possible, if at all, for the world to avert catastrophe is so slim, that it would be tragic for people who wish to exert themselves in the cause of peace to waste their energy, as one of them put it, "barking up the wrong tree."

A crude or naive form of the economic interpretation of history(4) sometimes used to explain investment friction between capital-exporting powers, posits some such pattern as the following in the origin of these disputes: Bankers, business men, speculators, scour the earth looking for profitable opportunities to invest what is often called "surplus capital."(5) They seek railway concessions in China, establish banks in Persia, acquire mining rights in Morocco. In all these undertakings they seek, and secure, the support of their national governments. Rival investors of different nationalities are attracted by these supposedly lucrative opportunities, and they enter into competition, each persuading his government to back him diplomatically in his quest for profits. Soon the governments find themselves involved in controversies over the investment opportunities sought by their respective capitalists, or over the protection of capital investments once made. Pushed on by the influence of profit-seeking investors, who continue to demand vigorous support of their financial enterprises, the governments come to sharp political clashes, which may prepare the way for war.(6)

Now, there is nothing logically wrong with this theory. It is perfectly plausible. And events very close to the description it provides have occurred in the actual world. But the facts of investment friction between capital-exporting nations have usually been a good deal more complicated than this theory implies, and especially is this true of those difficulties that have been really serious threats to international peace. The vice of this crude theory is its dangerous over-simplification---dangerous because the half-truths it presents in easy tabloid form divert attention from some vital factors in investment friction and lead to false conclusions regarding the policies of control that might promise most success in minimizing such friction.

The theory rests on half-truths in three important respects. In the first place, it is true that investors do put pressure on governors to influence state policy in ways favorable to the formers' profit interests. The objectives and the methods of such pressure have been analyzed in Chapters 6 and 8. But it is definitely untrue that many cases can be found where immediate pressure of this kind has pushed governments so far as to provoke really serious clashes with other strong powers. An explanation for that fact has been offered in Chapter 13. In the second place, it is true that the ends sought by governmental policies which lead to clashes with other governments often do include expansion of opportunities for the profitable investment of capital. It is not true, however, that the impulse to such purposes on the part of the governors comes necessarily, or even usually, from the pressure of persons with direct economic interest in investment outlets. As a matter of fact, it is a striking circumstance that governments, journalists, colonial zealots, and patriotic societies have often been more avid than the owners of capital in the promotion of investments abroad. Third, and finally, while it is true that the immediate economic interests of rival investing groups come into conflict over desirable investment opportunities, the crude theory fails to give adequate weight to the fact that such conflicts are ordinarily subject to solution with reasonable ease on the basis of the business techniques of compromise, buying and selling, so long as purely profit-making considerations are involved. If simply the direct pressure of profit-seeking business were behind the investment frictions between capital-exporting powers these would be much less dangerous. Business interests can be compromised much more readily than can strivings for national power, prestige, and glory.(7) The process by which the latter come to be bound up with the former is not adequately explained in the over-simplified theory we have been discussing.

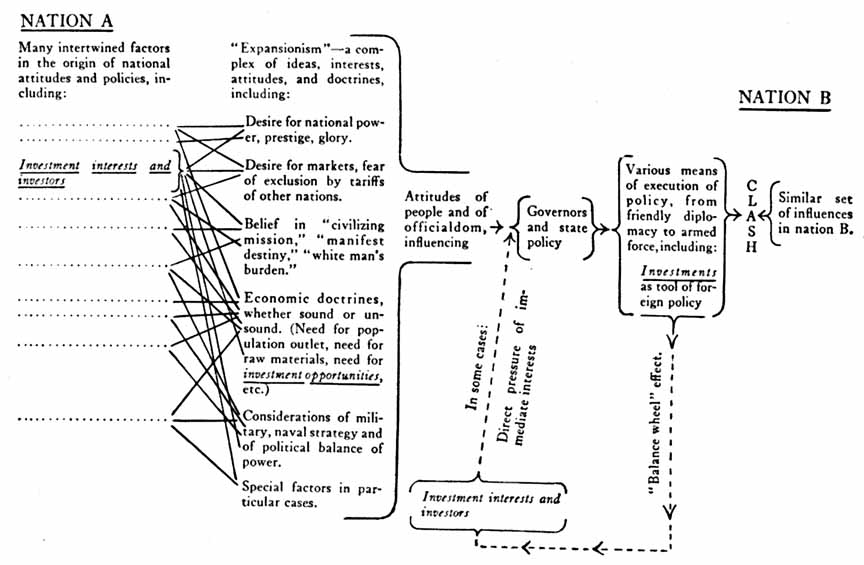

Some of the important elements in the development of investment friction between capital-exporting countries are indicated in the diagram above, which is offered as a closer approximation to the actual facts than the doctrine just criticized. It will be noted that private investments may enter the process described by this diagram at any one or all of four points: (1) Investors and investment interests may have a part in originating some of the complex of ideas, interests, attitudes, and doctrines here labelled "expansionism." This may be quite unconscious and unintentional, as by simply establishing contacts with previously unknown regions. On the other hand, investors or would-be investors may set out deliberately to encourage the development of an expansionist movement, by propaganda and other means. (2) The doctrine that the nation needs investment opportunities abroad for its "surplus capital" may be advanced as part of the expansionism complex. This doctrine may actually come from those who wish to invest capital, but probably more often it is a rationalization used by navy leagues, colonial societies, or foreign ministers in justification of their policies. (3) Investment interests and investors may exert direct pressure on the governors. This is the type of relationship between private investment and international friction emphasized by the over-simplified theory criticized above. While inadequate by itself, it is by no means to be neglected. It takes a subordinate position in this diagram because it never seems to be effective in bringing a really serious political clash between major capital-exporting powers except when acting in conjunction with some part of the expansionist complex. The expansionist complex, on the other hand, has often been effective in producing investment friction without the aid of direct pressure from immediate investment interests. (4) Investments may be used by the governors as a tool of foreign policy. Investments may likewise be used by colonial societies and similar organizations, or even by energetic individuals, as a means of fostering expansionist projects which the governors have not yet been persuaded to take over officially. In some cases this may be done with the connivance of the responsible governmental officials, in others as a means of forcing them into a desired policy. (Lines showing these last relationships do not appear on the diagram; they would make it too complicated.) The line running from "Investments as tool of foreign policy" to "Investment interests and investors," where it joins the direct pressure on the governors and state policy, indicates that once private investments have been brought into a given situation as tools of foreign policy they acquire interests of their own and henceforth are likely to exert direct pressure on the government's decisions. This has been described earlier as the "balance-wheel" effect of private investments used as instruments of diplomacy.

If the reader desires a typical pattern of events for cases in which investment friction has arisen between capital-exporting countries, the following might be offered as more realistic than the over-simplified one criticized earlier in this chapter: Explorers, traders, travelers, and missionaries establish contact with an undeveloped region. They spread reports, often extravagant, of its wealth and potentialities. Colonial and geographic societies may even be formed, and if so their membership will consist not only of business men with interests in foreign trade or investment, but their most active elements are likely to be ardent young journalists, military and naval men, members of the aristocracy, romantic geographers, explorers, government officials, "national" economists, and nationalistic patriots in general. The government comes to be inspired by certain economic and political ideas which call for extension of the national sovereignty, or at least the national influence, over foreign territories. In the meantime, a few citizens have established more or less important economic interests, mainly of a trading nature, in the undeveloped country and have perhaps applied for concessions. Their home government now gives these citizens energetic support, urges others in, perhaps subsidizes some firms. It takes every opportunity to assert the national interest, economic and political, in the territory now vaguely marked out for national expansion. It makes diplomatic bargains with other powers looking toward ultimate control of the territory. Bankers who hesitate to risk funds in the region are urged to do so on patriotic grounds. Concessions representing investment opportunities are extracted from the native government of the territory now being consciously "penetrated"---in many cases before any capitalists can be found who are willing to accept the "opportunities" so assiduously sought out by the diplomats. Meantime, some other great power has started to pursue similar ambitions in the same region, or has become alarmed lest the territory be seized by the first power and then closed to its traders and investors, or feels that the political balance of power is being disturbed, or that the acquisition of political influence in this region by the first power is a threat to "vital interests" of its own, such as lines of communication to existing colonies, strategic naval plans, and the like. This second power endeavors to oppose the process of penetration by political and economic means, often including the urging in of its own capitalists and demands for concessions to them. Thus political friction over investments and investment opportunities in the undeveloped country arises, and its intensity will depend largely upon the "vital" national interests thought to be at stake. A good many outside observers, whose attention is now drawn to the matter for the first time and who see the two powers quarreling over concessions, railways, and economic advantages, will at this point draw the obvious, but erroneous, conclusion that the main conflict is between the immediate economic interests of rival investing groups.

It is under circumstances approximately represented by this pattern that most of the dangerous crises between great powers over concessions and foreign investments have come into being. Some such chain of events led up to the clashes of the powers in Tunis, Morocco, Abyssinia, Persia, Korea, Manchuria, and various parts of tropical Africa. This is not the only pattern which has been followed in the origin of investment friction, however, and certainly not the only one which may be expected in the future. Inspection of the diagram presented above shows clearly that there are many possible combinations of the elements which seem to be common in investment friction cases, and they may enter in various sequences. A pattern which has been important in a number of cases is represented by the international friction over the Bagdad Railway. In this case the interests of the German promoters definitely preceded the political interest of their government and provided the occasion for its development. Once the government had turned its attention to the railway project and German publicists had begun to weave a nationalistic myth about it, however, the enterprise became much more of a political stake than was pleasing to the promoters themselves. German writers and writers in other countries, chauvinists of various lands---many of them quite unconnected with anyone having a direct economic interest in the Near East---read all sorts of political implications into it. Foreign governments opposed it, mainly for reasons connected with the balance of power, alliance politics, protection of "the road to India," though specific economic interests like those of the Lynch Brothers also stiffened the opposition. The result was the spectacle of German, French, and English financiers wanting to pool their resources under some sort of a working compromise which would remove political opposition, but prevented from doing so through many years by the. pressure of nationalistic sentiments in their various countries and by the political preoccupations of their foreign offices.

In order to put the immediate, economic conflicts of rival investing groups into proper perspective among the causes of the investment frictions which arise between capital-exporting powers, this chapter has dwelt at length upon the generalized description of the processes by which such friction originates. The complex of ideas, interests, attitudes, and doctrines here called "expansionism" has received much emphasis in this connection. In fact, the tendency of the argument---representing conclusions which seem unavoidable in view of the concrete evidence---has been to substitute expansionism for the pressure of immediate private investment interests as the villain of the drama, insofar as investment frictions between capital-exporting countries are concerned. But this is in one sense simply to push the question as to the rôle of private foreign investments one step further back, for expansionism has been pictured as the resultant of many social forces, among them some connected with private investment interests or the activities of private investors. To what extent has the pressure of capital for profitable opportunities abroad, or the influence of actual and would-be investors, been responsible for expansionism and thus indirectly for investment friction?

If we were to engage in a thorough investigation to ascertain inductively, on the basis of specific, historical materials rather than by the untested application of any dogma or doctrine, what factors have contributed to the development of expansionism in each of the great powers and what has been the rôle of private capital among these factors, it would require at least one volume in itself to present the relevant evidence and to analyze it critically. Even then, for most countries, the evidence would not be conclusive; that is, it would be of a sort that competent and objectively minded persons could still interpret differently in important aspects. This inheres in the nature of the question under discussion. Perhaps the causation of complicated social phenomena like expansionism can never be determined with certainty. Be that as it may, despite these reservations there are two conclusions which seem to emerge with sufficient distinctness so that they deserve mention here. First, the investment pressure in which we are interested cannot be regarded as an indispensable element in the causation of expansionism, for certain modern nations where such pressure has been absent or minimal have nevertheless developed most vigorous outward drives of a sort which we must accept as falling within our definition, since they have involved the use of investments as tools and have led to investment friction with other powers. Second, investment pressure has been a factor in the origin of expansionism in certain other countries, to a degree impossible to evaluate accurately, but differing from country to country and apparently quite important in some. In all such cases it has been intertwined with other factors of the most diverse kinds. A brief amplification of these two conclusions will bring to a close this chapter on investment conflicts between capital-exporting countries.

The pre-war histories of Russia and Italy lend no support whatever to the hypothesis that the pressure of "surplus capital" for investment abroad is an essential element in the origin of modern national expansionism. Tsarist Russia was capital-poor, a heavy borrower when possible, and yet it sprawled over Northern Asia, contested Korea and Manchuria with Japan, sought to extend its sway southward to Constantinople, and engaged in such an aggressive politico-economic penetration of Persia that England was alarmed for the safety of India. These were typical activities of the sort which has been called "capitalistic imperialism." Investments which were private in form, but really heavily subsidized by the Tsarist government, served as tools of penetration; they included banks, railroads, road construction, forestry companies, shipping and trading companies, and also loans to weaker states. Russia engaged actively in the scramble for concessions in the Far Fast and in the Middle East. And yet Russia had no "surplus capital" in any reasonable sense of that term; Russia had very little capital at all and borrowed heavily from abroad. Nor were Russian financiers putting pressure upon the government to get them investment opportunities abroad; the government was pressing the financiers, subsidizing them, to create political stakes abroad. Much of the capital used as a Russian diplomatic tool was borrowed in France. Lest it be suggested that Russian expansionism was therefore an expression of the outward push of French "surplus capital" it is well to point out that Russian governments had been engaging in expansionist politics for decades before the first loan was floated in France. The causes of Russian expansionism have to be sought in political ambition, dynastic megalomania, military lust for conquest. Capital was distinctly a tool, not a cause.

The case of Italy is only slightly less clear than that of Tsarist Russia. Italy, too, was a nation poor in capital, borrowing abroad for its own needs. Yet it engaged in the struggle for acquisition of territory and spheres of influence which characterized the decades before the World War. A rising spirit of nationalism seeking to assert itself in the. world, the quest for prestige and glory, were more effective causes of Italian conquest in Tripoli, the establishment of colonies elsewhere on the African coast, the attempt to extend Italian influence over Abyssinia, and the dispute over Tunis with France, than were any investment factors. The capital which served as a tool of penetration in Tunis and Tripoli had to be pushed in and subsidized. The opportunity to participate slightly in the Bagdad Railway enterprise, secured for Italy by its diplomats for political reasons, actually had to be taken up by so-called Italian capital of Greek origin.(8) Italy's aggressive expansionist tendencies before the World War developed without significant pressure from opportunity-seeking capital.

It can surely be concluded from these cases that the existence of "surplus" investment capital pressing for opportunities abroad is not a necessary element in the origin of nationalistic imperialism, colonialism, or---in the general term used here---expansionism. On the other hand, the quest for desirable investment opportunities has undoubtedly been a factor of varying magnitude in the development of expansionism on the part of other powers. In France, Jules Ferry and other expansionists believed (or at least said, as an argument for their colonial policy) that investment opportunities were needed abroad. Propaganda of this sort came primarily from statesmen and others who were already zealous colonialists, however, not from the bankers and would-be investors themselves. Doubtless it is part of the duty of a statesman to anticipate the needs of the business community and to make them vocal and effective in national policy even before the business community is conscious of them; in this sense French expansionism received part of its impetus from a desire for investment opportunities abroad. It is worth noting, however, that investments actually made in colonies were a small part of French capital exports before the war. The major factors in French expansionism appear to have been such things as these: the conviction that trade outlets were necessary for the industrial development of the country, coupled with the rise of protectionist tendencies in markets all over the world; the impulse to seek prestige, glory, a great place in the world, for the French nation; the desire to recover the injury to national pride inflicted in 1871; the conviction that France had a mission to spread its culture abroad. The desire for investment opportunities was present, at least in the minds of statesmen, but it was hardly among the most effective causes of French expansionism.

The interests of British private investors scattered over most of the world, especially investments connected with trade, undoubtedly contributed mightily to the resurgence of British expansionism in the late nineteenth century. Their mere existence tended to turn business and political interests outward; they provided ready footholds for political operations at almost any point on the earth's surface without the necessity for creating "economic" interests out of whole cloth, as the Russians had to do; they were characteristically accompanied, unlike the investments of the French, by outposts of home enterprises and by personnel from home, which made their political significance quite different. The tendency of private capital to seek out new opportunities abroad was, therefore, an important element in modern British expansionism, along with other important factors, such as the long and still active tradition of colonialism, the naval tradition, the influence of the colonial official class, the quest of careers by younger sons of the aristocracy, missionary enterprise, the search for export markets, and the psychic satisfaction which comes from seeing one's own country cover a larger and larger portion of the world map.

The origin of German expansionism offers the most interesting case of all, for the influences at work came to a focus in shaping the policy of one dominant statesman, Bismarck. In the forces which played upon Bismarck, inducing the famous shift from his earlier maxim that Germany had only continental interests to his later studied attempt to promote German expansion in Africa and the South Seas, one sees reflected the social forces which were molding the destiny of the nation. Did the interests and influence of those who wished to place private capital profitably abroad have an important part in this shift? The answer is that they did. The powerful influence of Bismarck's banker friends, von Hansemann and Bleichröder, was exerted in favor of a colonial policy, and the practical enterprises of great merchants and shippers like Godeffroy and Woermann furnished the immediate occasions for early demonstration of the new state attitude. As in all the other cases, however, investment interests seeking opportunities and protection represented but one among a number of significant factors in the rise of expansionism. Probably the single most important consideration influencing Bismarck resulted from the rise of protectionism in the latter part of the nineteenth century and its application by other powers to their possessions. The rise of protectionism meant that a nation without colonies would have to fear exclusion from markets for its industries, limitation of trading and investment opportunities, unless it, too, entered the race for possessions and spheres of influence abroad. In the last analysis, however, even in Germany where economic forces were particularly evident in the origin of expansionist tendencies, the colonial movement was most easily justified in the eyes of the people on the basis of patriotic pride and national prestige.(9)

The annexation of Hawaii by the United States was due in large part to the activities of American plantation owners---therefore, of private investment interests. Their main economic interest, however, was in obtaining tariff preferences for their products in the United States; so that here, too, the protectionist policy of nations was an important factor. Furthermore, the economic interests of the Hawaiian investors did not suffice in themselves to bring about annexation; after at first refusing to take over the islands, the government of the United States finally did so in the nationalistic enthusiasm aroused by the Spanish-American War. The causes of this war, and of the expansionism exhibited in connection with it, have been laid at the door of private investment interests---on the whole, erroneously. Their rôle was slight compared with that of the interests of the "yellow" press and of other internal influences in American life which made for chauvinism. Certainly, investment interests in the Caribbean countries have recently contributed significantly to American political dominance there, though strategic interests connected with naval power, defense of the Panama Canal, and the traditional policy of the Monroe Doctrine were probably more important in turning the political attention of the United States government to the region. The Caribbean seems to offer one of the best illustrations of the "balance-wheel" effect of private investments. Coming in, on the whole, after the political interest, they have tended to make it more intense and permanent. American political interests in the Far East were closely connected with trade from the first, and more recently investments have come to share the importance of trade in conditioning policy. But there has been no important tendency for the United States to adopt an expansionist program there. The conclusion with respect to the United States must be much like those reached for France, England, and Germany: private foreign investments have figured in national expansionism, but as one among many factors, some of which have been more important than the investment influence.

Finally, Japan must be considered. Certainly, in this case, though the forces producing Japanese expansionism may be largely economic in the broad sense of that term, the direct influence of private profit-motivated enterprise seeking either investment opportunities or protection abroad has not been a very significant item in the development of that expansionism. Rather, Japan, like Russia and Italy, has borrowed abroad and pushed subsidized enterprises into coveted territory in order to establish political stakes. Perhaps Japanese statesmen have been influenced in part by the consideration that some time in the future the country will be in need of profitable outlets for "surplus capital" abroad, but even this must be counted a minor factor in comparison with such forces as the concern over population pressure on the standard of living, the belief that raw materials lacking in Japan must be secured by national expansion abroad, the social and political prestige of the military class, and nationalistic pride such as that which has driven forward the colonial enterprises of other states.

.

To recapitulate the conclusions reached in this chapter: There are two direct economic conflicts between rival lending groups. The first is represented by competition for the most attractive investment opportunities, the second by conflict over precedence of claims where there are joint creditors of the same debtor. Conflicts of the second type have hitherto not been very significant politically; their importance may increase if governmental control of all payments abroad continues to be practised in many countries. Conflicts of the first type have contributed to the origin of political friction between nations, but the actual process by which they enter into political situations is a good deal more complicated than has been assumed in certain naïve theories. Many other factors are more important in the immediate causation of international investment friction than the direct economic interests of investors or would-be investors. "Expansionism" is a term which lumps together a variety of such factors. Expansionism itself may be caused, in part, by the economic interests of certain groups in investments or investment opportunities abroad, but it may also arise, and has arisen in several cases, under circumstances which make it clear that private investment interests have had no part in its causation.